Type "loans for bad credit" into a search engine and you'll find two kinds of results: lenders promising miracles, and articles telling you it's hopeless. Both are wrong. A rough credit score narrows your options and raises your cost — but it doesn't lock the door, because score is only one of the things lenders actually evaluate. Here's what's really happening behind an approval decision, and how to put your strongest foot forward.

What "Bad Credit" Actually Means

Most lenders using FICO scores treat roughly 580–669 as "fair" and below 580 as "poor." Landing there usually comes from some mix of late payments, high card balances, collections, or simply a thin file with little history. Here's the part the doom-articles skip: those bands describe your past repayment record — they say nothing about whether your current income can support a new, modest payment. That's exactly the gap income-based lenders work in.

What Lenders Really Look At (Beyond the Score)

- Income and its stability. Regular paychecks, benefits, or consistent self-employment deposits matter more than any three-digit number.

- Ability to repay. The core question: after rent, utilities, and existing obligations, does the proposed payment realistically fit? Responsible lenders decline loans that don't — that's protection, not rejection.

- Banking history. An active checking account in good standing signals stability that a score can't capture.

- Requested amount. A $600 request against a $2,400 monthly income reads very differently from a $5,000 one.

This is why at Cash Store all credit types are considered: underwriting starts from income and ability to repay. Approval is never guaranteed — but a bruised score alone won't end the conversation.

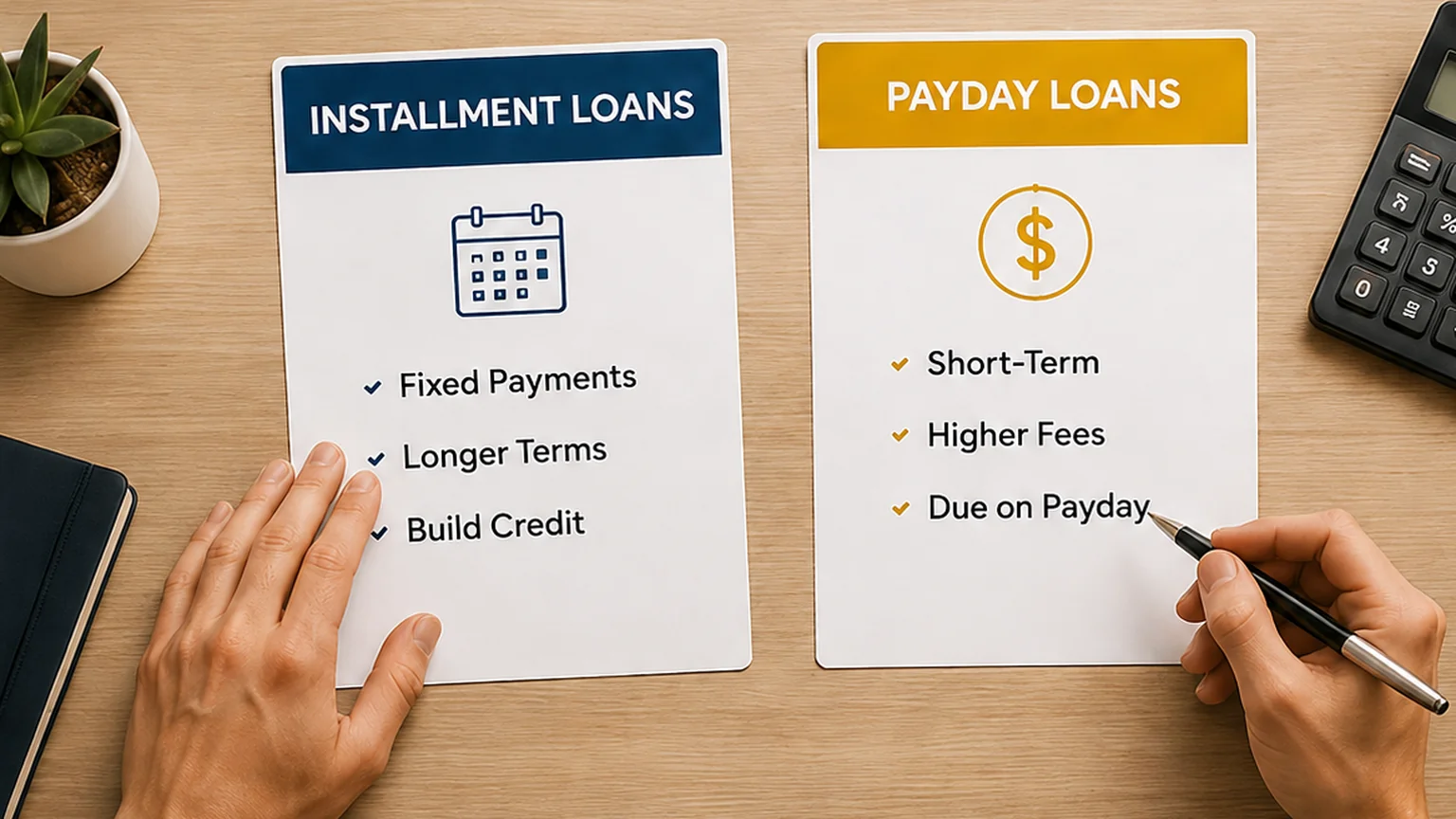

Your Realistic Options with Rough Credit

- Installment loans ($500–$5,000): fixed scheduled payments over 3–12 months; the go-to for larger one-time expenses.

- Cash advances ($200–$1,000): one repayment on payday for small, short gaps.

- Title-secured loans (up to $5,000): if you own your car outright, its value carries weight your score doesn't have to.

- Lower-cost routes worth checking first: credit union Payday Alternative Loans (PALs), employer paycheck advances, payment plans from the biller, and local assistance programs — all typically cheaper than short-term credit.

How to Improve Your Approval Odds

- Ask for less. The single most effective move — smaller requests are easier to approve and cheaper to repay.

- Have documents ready. ID, a recent pay stub, and bank details turn a stalled application into a same-day one.

- Apply with your main bank account. Months of steady deposits are your best evidence of stability.

- Don't shotgun applications. A burst of hard-inquiry applications across many lenders can drag your score further down.

Does checking my rate hurt my credit? Pre-qualification typically uses a soft inquiry, which doesn't affect your score. Read our guide to what "no credit check" really means for the full soft-vs-hard breakdown.

Red Flags: When "Bad Credit OK" Means "Scam"

- "Guaranteed approval" — real lenders underwrite; guarantees are bait.

- Upfront fees before funding — the signature of advance-fee fraud.

- Pressure to decide "right now" — legitimate offers survive a night's sleep.

- No license information — a lender who can't show state licensing (see our Rates & Licenses) isn't a lender.

Ready to see your real numbers?

Check what you qualify for in about 5 minutes — free, no obligation, and every cost in writing before you decide.

The Bottom Line

Bad credit makes borrowing more expensive — it doesn't make it impossible, and it doesn't make you a bad bet. Lead with your income story, borrow the smallest amount that solves the problem, repay on schedule, and each loan becomes a small brick in rebuilding the score that started this whole search.