You need cash before payday, you search for a quick loan, and two options keep coming up: installment loans and payday loans. They look similar from a distance — both are fast, both work with imperfect credit, both put money in your account quickly. But they're built on opposite repayment structures, and picking the wrong one for your situation is the most common (and most expensive) mistake in short-term borrowing.

Here's the complete comparison, with real numbers.

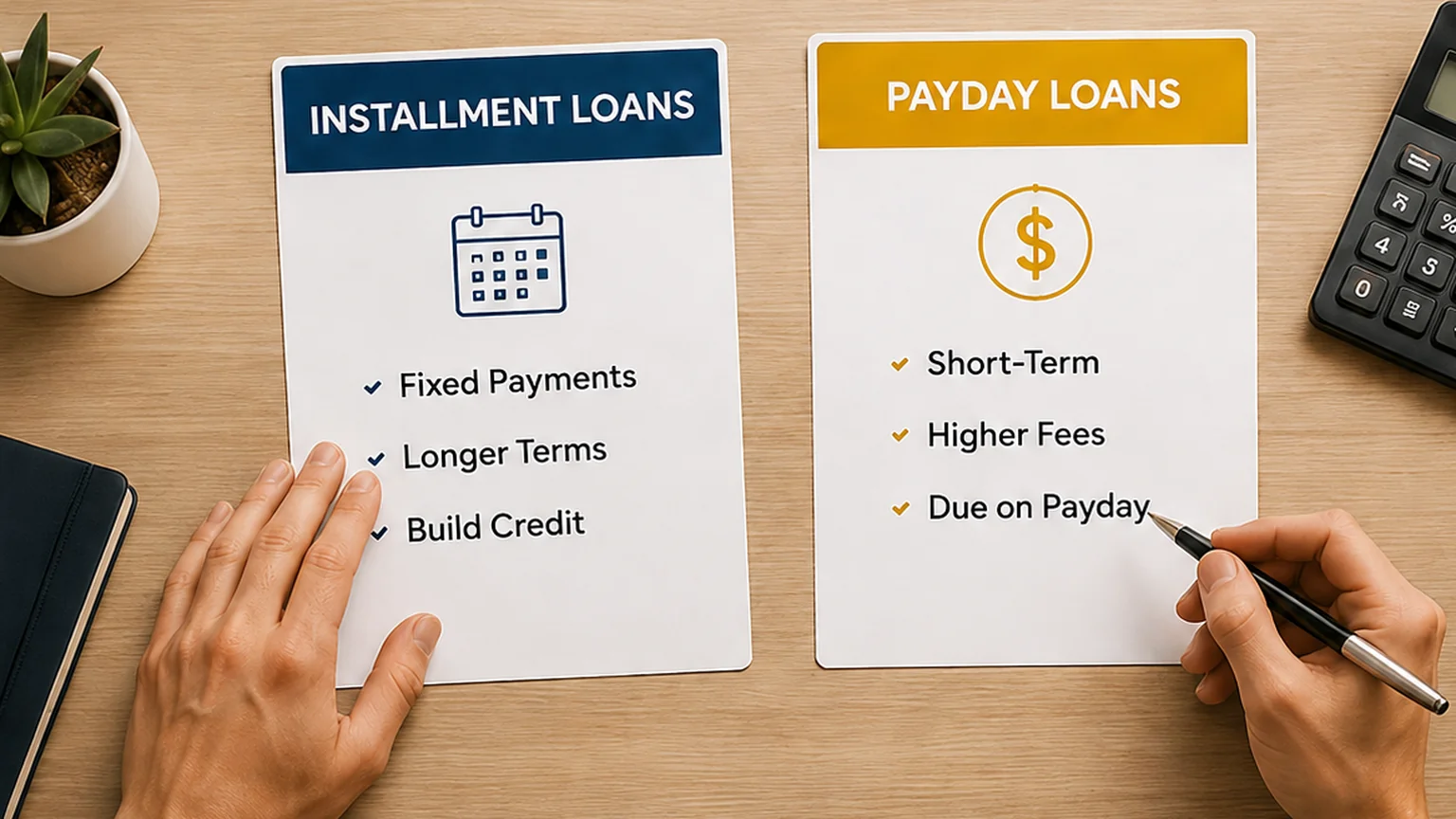

What Is an Installment Loan?

An installment loan gives you a fixed amount — $500 to $5,000 at Cash Store — that you repay in equal, scheduled payments over a set term, typically 3 to 12 months. Every payment includes principal and interest, so the balance falls with each one, and the payment amount never changes. You know the total cost, the number of payments, and the payoff date before you sign.

What Is a Payday Loan?

A payday loan — called a cash advance at Cash Store — is a small loan ($200–$1,000) repaid in one single payment on your next payday, usually within two to four weeks. Instead of interest that accrues over months, you pay one flat fee. Borrow $500 with a 15% fee, and you repay $575 on payday. Simple — as long as your paycheck can absorb the whole amount at once.

The Key Differences, Side by Side

| Installment Loan | Payday Loan / Cash Advance | |

|---|---|---|

| Typical amount | $500 – $5,000 | $200 – $1,000 |

| Repayment | Fixed payments over months | One lump sum on payday |

| Term | 3 – 12 months | ~2 – 4 weeks |

| Pricing style | APR accruing over time | One flat fee |

| Budget impact | Smaller, predictable hits | One large hit on payday |

| Early payoff | Saves interest (no penalty) | Little to save — fee is fixed |

| Biggest risk | Committing to months of payments | Re-borrowing if payday can't cover it |

What They Really Cost: Two Honest Examples

Installment: a $1,000 loan at 189% APR over 6 months means about 12 bi-weekly payments of $127.72 — a total repayment of $1,532.64. Expensive compared with a bank loan, but each individual payment is small enough to plan around, and paying early cuts the total.

Payday: a $500 advance with a 15% fee costs $75 — you repay $575 in two weeks. That sounds cheaper, and in absolute dollars it is. But expressed as an APR, a two-week 15% fee works out to roughly 390% — the structure only makes sense because it's over in weeks, not months.

The trap to avoid: the payday structure fails when your paycheck can't absorb the full repayment and you re-borrow to cover it. Back-to-back advances turn a two-week fee into a rolling monthly cost — the single most expensive pattern in consumer lending. If there's any doubt one paycheck can handle it, the installment structure exists precisely for you.

Which One Should You Choose?

- Choose a payday loan / cash advance when: the expense is small (under ~$1,000), truly one-time, and your next paycheck can comfortably cover the full repayment after your normal bills.

- Choose an installment loan when: you need more than $1,000, or you'd rather protect your budget with smaller fixed payments — even if it means paying interest over a longer period.

- Choose neither when: the shortfall repeats every month. No loan structure fixes an income gap — start with our responsible lending resources and lower-cost alternatives like credit union PALs.

Ready to see your real numbers?

Check what you qualify for in about 5 minutes — free, no obligation, and every cost in writing before you decide.

The Bottom Line

Installment loans and payday loans aren't better or worse — they're different tools. Payday-style advances are for small gaps one paycheck can close; installment loans are for bigger expenses that need to be spread out. Match the structure to your paycheck reality, borrow only what the problem actually costs, and read the total repayment figure — not just the fee — before you sign. That one habit will save you more than any rate shopping.